UTICAJ USVAJANJA MEĐUNARODNIH RAČUNOVODSTVENIH STANDARDA NA KORUPCIJU: TRANSPARENTNOST I FINANSIJSKA ODGOVORNOST

Apstrakt

Transparentno poslovanje obezbeđuje jasan uvid u sve faze poslovnih aktivnosti, čime omogućuje njihovo jasno razumevanje. Transparentnost je, istovremeno, prepreka pojavama korupcije, koja nastaje korišćenjem službenog ili društvenog položaja ili uticaja radi sticanja nedozvoljene koristi. Instrumenti za borbu protiv korupcije ugrađeni su u same standarda. MRS JS su dizajnirani da globalno poboljšaju transparentnost i odgovornost entiteta u javnom sektoru. Efektivnost MRS JS u borbi protiv korupcije zavisi od institucionalnog konteksta i faze implementacije. Ovaj rad ima za cilj da ispita kako implementacija IPSAS može doprineti smanjenju korupcije. U radu su primenjeni konceptualni i analitički pristup.

Članak

Introduction

Organizational governance encompasses establishing relationships that ensure the achievement of outcomes defined by stakeholders. In the public sector, governance should guarantee that desired results consistently serve the public interest. Acting in the public interest requires commitment to ethical values, respect for the rule of law, and an environment open to comprehensive engagement of all stakeholders.

The main objective of public sector entities lies in improving or maintaining the well-being of citizens, which distinguishes them from the private sector, which is profit-oriented. For instance, the implementation of social policy may at times require giving greater weight to issues of equality and fairness than to the financial performance of activities aimed at achieving those goals. Public sector entities are often obliged to reconcile the interests of various groups in society. They hold the authority to regulate entities from certain economic sectors and to protect and promote the interests of citizens, consumers, and other stakeholders (IFAC & CIPFA, 2014).

The paper is structured as follows. The first section focuses on examining IPSAS as a component of the public sector environment. The second section explores IPSAS as a tool for combating corruption. Conclusions are presented in the last section.

IPSAS as a component of the public sector environment

The emergence and development of International Public Sector Accounting Standards (IPSAS) is a relatively recent phenomenon that was formally institutionalized in 1986 with the establishment of the International Public Sector Accounting Standards Board (IPSASB, 2023a) by the International Federation of Accountants (IFAC). The goal of adopting IPSAS has been, and continues to be, the reform of public sector financial reporting in line with modern principles of public sector governance, directed toward transparent, clear, efficient, and effective use of public resources and accountability to citizens and other stakeholders served by the public sector.

The IPSASB formulated these standards with the long-term aim of replacing the traditional cash-based reporting system in the public sector with an accrual-based system that captures all economic events, i.e., all transactions, regardless of whether they are completed with cash flows. In other words, the objective of these standards is to replace the traditional cash accounting system in the public sector with accrual accounting, which is widely applied in the private sector (Pina, Torres, 2003; Olson et al., 2000). The cash-based accounting system does not provide comprehensive information for decision- making, as it focuses solely on recording monetary transactions. “The development of accounting theory and practice, although not very dynamic, has influenced financial accounting” (Nićin, 2024). “Understanding the information system relevant to financial reporting is a matter of the auditor's professional judgment” (Zekić, 2015).

In addition to IPSAS, the IPSASB also issued a specific standard for financial reporting on a cash basis, IPSAS: Financial Reporting under the Cash Basis of Accounting, which sets out mandatory requirements and recommended guidelines for disclosure of transactions. This standard encourages entities to voluntarily disclose accrual-based information, even if their primary financial statements are prepared under the cash basis of accounting.

One of the key drivers for IPSAS adoption is the requirement for operational transparency. Transparent operations provide clear insight into all phases of business activities, thereby enabling more detailed knowledge of such activities and their clear understanding. Consequently, transparency increases the number of stakeholders and stimulates their active participation in public engagement. At the same time, transparency acts as a barrier to corruption, which arises from the misuse of official or social position or influence for the purpose of gaining illicit benefit (Law on the Prevention of Corruption, 2022). “Certain positions in the financial statements are a frequent target of fraudsters” (Gogić, 2022). Forensic accounting is defined in the literature as an interdisciplinary field that combines accounting, auditing and investigative techniques in order to detect, prevent and resolve financial fraud. This topic was the subject of research by various authors, who emphasized its key role in the fight against corruption, abuses and other forms of financial crime (Mitrić et al., 2012; Ilić, Anđelić, 2017; Cvetković, Bošković, 2018; Đorđević, Mitić, 2020; Knežević et al., 2021a; Knežević et al., 2021b; Knežević et al., 2022; Janković et al., 2023; Mitrović et al., 2025; Milojević et al., 2025; Milojević, 2025, Matejić et al., 2025).

IPSAS as an anti-corruption instrument

The literature contains a considerable body of research on whether the application of IPSAS can reduce corruption in the public sector. Much of the literature supports the claim that accrual-based accounting systems reduce corruption. There is also evidence that the application of IPSAS, allowing the use of cash-based accounting, as an initial step toward the adoption of accrual-based IPSAS, helps bring corruption under control. Studies by Tawiah (2023), Hamed-Sidom et al. (2022), and Cuadrado- Ballasteros et al. (2020) confirmed that accrual-based accounting systems mitigate corruption. Research results on the impact of IPSAS adoption on governance quality and corruption control, focusing on three Southern European countries – Spain, Portugal, and Italy, indicate that in countries with a strong institutional framework (Spain), IPSAS adoption ensures a high level of financial transparency, governance, and corruption reduction. Partial IPSAS adoption (Portugal) and the ongoing transition of the Italian public administration toward IPSAS show less favorable outcomes (Maali, Morshed, 2025). Findings also suggest that increased clarity reduces information asymmetry between government authorities and the public, compelling public officials to act in public interest (Scannell, Tawiah, 2024).

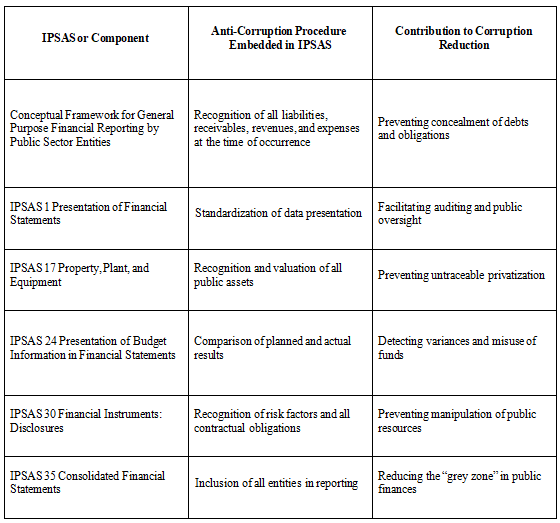

Concrete anti-corruption mechanisms embedded in IPSAS include: the requirement to recognize all liabilities, receivables, revenues, and expenses at the time they occur; standardized presentation of all data; disclosure and valuation of total public assets; recognition of risk factors from contractual obligations; consolidated reporting; and more. These requirements enhance control over public resources, reduce opportunities for manipulation, and facilitate the functioning of oversight processes as well as financial and performance auditing. Standardized data, accrual accounting, and transparency enable precise analysis of cash flows, assets, liabilities, and budget variances, thereby significantly strengthening institutional resilience against misuse (Beke Trivunac et al., 2024).

Table 1: Examples of IPSAS - Embedded Procedures Contributing to Corruption Reduction

Source: Authors´ own elaboration

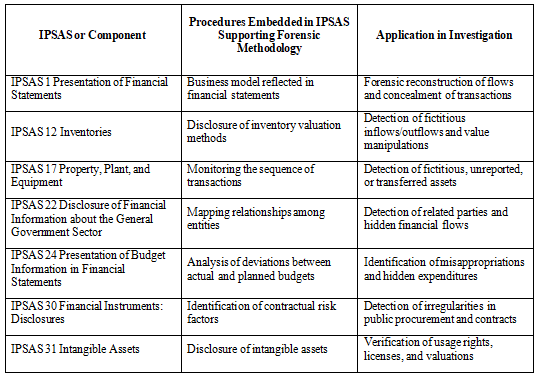

Another dimension of IPSAS's contribution to corruption reduction lies in creating conditions that facilitate forensic auditing processes. The increased effectiveness and efficiency of forensic investigations arise from several factors:

(1) Transparency and accountability required by IPSAS create an environment in which abuses are easier to detect and prove.

(2) Standardized data provide a reliable foundation for forensic analysis. IPSAS ensures consistent, accrual-based data on assets, liabilities, revenues, and expenses. Forensic investigators use these data to identify anomalies, such as misclassified expenditures, undisclosed assets, and mismatches between budgeted and executed figures.

(3) IPSAS 24 Presentation of Budget Information in Financial Statements requires a comparison of planned and actual budgets, which enables the detection of variances and the reconstruction of cash flows in suspected cases of misuse.

(4) IPSAS 17 Property, Plant, and Equipment requires detailed recognition of fixed assets. Forensic investigations use this data to uncover fictitious or non-existent assets and track transfers of assets between entities.

(5) In combination with systems that integrate public sector functions: budgeting, accounting, procurement, asset management, and human resource management – into a unified digital platform, IPSAS facilitates transparent and consolidated management of public finances. Such digital platforms are often developed during the transition process to new standards.

IPSAS have the capacity to illuminate what was previously hidden, and that is the first step toward accountability to citizens and other stakeholders.

Table 2: Examples of IPSAS - Embedded Procedures Facilitating Forensic Investigations

Source: Authors´ own elaboration

IPSAS never operate in isolation. Their effectiveness depends on institutional will, auditing capacity, and public access to information. According to the Framework for Ethical Reporting in the Public Sector (International Federation of Accountants, 2023b), enhanced stakeholder engagement, stable and reliable oversight of operations and performance, and monitoring of those primarily responsible for determining the strategic direction, management, and accountability of entities lead to more effective interventions and better outcomes for the public as a whole.

Conclusion

The IPSAS accounting framework is designed to globally enhance the transparency and accountability of public sector entities through the application of accrual-based accounting. Their effectiveness in combating corruption depends on the institutional context and the stage of implementation.

Anti-corruption instruments are embedded within the standards themselves. Therefore, the introduction of IPSAS is associated with strengthening institutional resilience. The application of IPSAS simultaneously enhances financial reporting. It increases operational transparency in public sector entities, thereby laying the foundation for a more effective fight against corruption in the public sector.

It should be noted that the positive effects of IPSAS implementation do not occur automatically but depend on the presence of appropriate complementary factors, including institutional readiness, political stability, the quality of the legal framework, and the adequate education and capacity of accounting and auditing services.

Reference

2.Cuadrado-Ballesteros, B., Citro, F., & Bisogno, M. (2020). The role of public-sector accounting in controlling corruption: An assessment of Organisation for Economic Co- operation and Development countries. International Review of Administrative Sciences, 86(4), 729–748.

3.Cvetković, D., & Bošković, V. (2018). Pojavni oblici kreativnog računovodstva i najčešće manipulacije u finansijskim izveštajima. Oditor, 4(2), 81-92. https://doi.org/10.5937/

4.Đorđević, S., & Mitić, N. (2020). Alternativni računovodstveni postupci, kreativno računovodstvo i lažno finansijsko izveštavanje. Oditor, 6(2), 21-

37.https://doi.org/10.5937/Oditor2002021D

5.Gogić, N. (2022). Prevare u finansijskim izveštajima. Oditor, 8(1), 7-35.

https://doi.org/10.5937/Oditor2201007G

6.Hamed-Sidhom, M., Hkiri, Y., & Boussaidi, A. (2022). Does IPSAS adoption reduce corruption’s level? New evidence from ODA beneficiary countries. Journal of Financial Crime, 29(1), 185–201.

7.Ilić, M., & Anđelić, S. (2017). The role of computerized accounting information system in

detecting accounting errors and accounting fraud. BizInfo Blace, 8(1), 17-

30. https://doi.org/10.5937/bizinfo1701017I

8.International Federation of Accountants, & Chartered Institute of Public Finance and Accountancy (IFAC & CIPFA). (2014). International framework: Good governance in the public sector. IFAC and CIPFA. https://www.ifac.org

9.International Federation of Accountants. (2023a). Framework for ethical public sector reporting. IFAC. https://www.ifac.org

10.International Public Sector Accounting Standards Board. (2023b). Preface to International Public Sector Accounting Standards. International Federation of Accountants. https://www.ifac.org

11.Janković, B., Knežević, S., & Milojević, S. (2023). Uloga računovodstvenog forenzičara u krivičnom postupku. Revizor - časopis za upravljanje organizacijama, finansije i reviziju, 26(101), 1–9. https://doi.org/10.56362/Rev23101001J

12.Knežević, S., Milojević, S. & Špiler, M. (2021b). Edukacija o forenzičkom računovodstvu i veza s praksom. Revizor - časopis za upravljanje organizacijama, finansije i reviziju, 24(95- 96), 35–49. https://doi.org/10.5937/Rev2196035K

13.Knežević, S., Milojević, S., & Paunović, J. (2021a). Razvoj forenzičkog računovodstva i izazovi u savremenom okruženju, Revizor - časopis za upravljanje organizacijama, finansije i reviziju, 24(95-96), 77–90. https://doi.org/10.5937/Rev2196077K

14.Knežević, S., Obradović, T., & Milojević, S. (2022). Upravljanje rizikom od pojave korupcije u sektoru odbrane. Revizor - časopis za upravljanje organizacijama, finansije i reviziju, 25(99), 21–34. https://doi.org/10.56362/Rev2299021K

15.Law on the Prevention of Corruption. (2019–2022). Official Gazette of the Republic of Serbia, Nos. 35/2019, 88/2019, 11/2021 – Authentic Interpretation, 94/2021, 14/2022.

16.Maali, B. M., & Morshed, A. (2025). Impact of IPSAS adoption on governance and corruption: A comparative study of Southern Europe. Journal of Risk and Financial Management, 18(2),

67. https://doi.org/10.3390/jrfm18020067

17.Matejić, T., Knežević, S., Milojević, S., Adamović, M., & Milošević, M. (2025). Forensic accounting in higher education in the republic of Serbia: assessing students’ needs for the introduction and design of educational programs in this field. BizInfo Blace, 16(2), https://doi.org/10.71159/bizinfo250023M

18.Milojević, S. (2025). Forensic accounting and taxation, Megatrend revija, 22(1), 1-16.

19.Milojević, S., Matejić, T., Milošević, M., & Resimić, M. (2025). Towards integrating forensic accounting in university curricula: Evidence from student perceptions. Journal of process management and new technologies, 13(3-4), 29-43.

20.Mitrić, M., Stanković, A., Lakićević, A. (2012). Forenzičko računovodstvo – karika koja nedostaje u obrazovanju i praksi. Management, 17(65) 41-50.

21.Mitrović, A., Knežević, S., & Milojević, S. (2025). Specifičnosti uloge interne kontrole u prevenciji prevara u hotelskim preduzećima. Revizor - časopis za upravljanje organizacijama, finansije i reviziju, 28(3 (111). https://doi.org/10.46793/Rev25111.069M

22.Nićin, S., Cvijić Rodić, J., Rodić, Lazić, S. (2024). The role of the accounting information system in modern business, Akcionarstvo – časopis za menadžment i pravo, 30(1), 165-175.

23.Olson, O., Humphrey, C., & Guthrie, J. (2000). Caught in an evaluatory trap: The dilemma of “public services” under NPFM. EIASM International Conference on Accounting, Auditing and Management in Public Sector Reforms.

24.Pina, V., & Torres, L. (2003). Reshaping public sector accounting: An international comparative view. Canadian Journal of Administrative Sciences / Revue Canadienne des Sciences de l’Administration, 20(4), 334–350.

25.Scannell, S., & Tawiah, V. (2024). A thematic literature review on International Public Sector Accounting Standards (IPSAS). Public Organization Review, 24, 1053–1075. https://doi.org/10.1007/s11115-024-00773-1

26.Tawiah, V. (2023). The impact of IPSAS adoption on corruption in developing countries.

Financial Accountability & Management, 39(1), 103–124.

Zekić, (2015). Kontrola i revizije u javnom sektoru, Akcionarstvo, 21(1), 23-33

Objavljeno u

Vol. 31, No. 1, 2025.

Ključne reči

Licenca

Ovaj rad je objavljen pod Creative Commons Attribution 4.0 International (CC BY 4.0).

Autori zadržavaju autorska prava nad svojim radom.

Dozvoljena je upotreba, distribucija i adaptacija rada, uključujući i u komercijalne svrhe, uz obavezno navođenje originalnog autora i izvora.

Zainteresovani za slična istraživanja?

Pregledaj sve članke i časopise