UNEMPLOYMENT CONVERGENCE IN THE EUROPEAN UNION: CRISIS ADJUSTMENT AND RECOVERY DYNAMICS

Abstract

This study examines unemployment convergence across the 27 member states of the European Union during the post-crisis decade. Using annual panel data covering the period 2010–2019, the analysis investigates whether labor market disparities narrowed following the sovereign debt crisis and during the subsequent recovery phase. A fixed-effects framework is employed to test for β-convergence in unemployment rates, complemented by sub-period estimations that distinguish between the crisis-adjustment phase (2010–2013) and the recovery period (2014–2019).

The results indicate statistically significant unemployment convergence throughout the decade. Convergence dynamics were stronger during the immediate post-crisis adjustment phase, with an estimated annual speed of adjustment of approximately 20 percent, and remained present - though more moderate - during the recovery period. These findings suggest that EU labor markets exhibited systematic mean reversion following the crisis, contributing to a gradual reduction in cross-country disparities in unemployment rates. The evidence is robust to alternative specifications and supports the view that labor market integration mechanisms intensified during periods of macroeconomic stress.

Overall, the study provides empirical evidence of dynamic labor market convergence within the European Union, highlighting the differentiated adjustment patterns between crisis and recovery phases.

Article

1. Introduction

The question of convergence has remained central to modern macroeconomics since the revival of growth theory in the early 1990s. Within the neoclassical framework, economies are expected to converge toward their steady-state equilibria conditional on structural characteristics such as savings behavior, demographic dynamics, and institutional settings (Barro & Sala-i-Martin, 1992, 2004). While the bulk of the empirical literature has focused on income convergence, the convergence concept has increasingly been applied to other macroeconomic variables, including productivity, inflation, fiscal balances, and labor market indicators.

Unemployment, in particular, represents a critical dimension of economic integration within the European Union (EU). Persistent cross-country disparities in unemployment rates raise questions about the effectiveness of common market mechanisms, monetary coordination, and structural reforms. Following the global financial crisis and the subsequent sovereign debt crisis, EU member states experienced highly asymmetric labor market shocks. Southern economies such as Greece and Spain faced dramatic surges in unemployment, while core economies exhibited comparatively stable labor market conditions. These divergences revived concerns regarding structural imbalances within the euro area and the broader EU framework.

Empirical research on convergence has progressively moved beyond homogeneous steady-state assumptions. Contributions incorporating heterogeneity and transitional dynamics emphasize that convergence may occur conditionally and may differ across sub-periods characterized by macroeconomic stress or stabilization (Durlauf & Johnson, 1995; Islam, 1995).

Recent empirical studies have examined convergence patterns within the EU using panel methodologies and club convergence approaches. Evidence suggests that while income convergence within the EU remains incomplete, periods of macroeconomic stress may induce stronger adjustment dynamics (Phillips & Sul, 2007; Próchniak & Witkowski, 2012). However, comparatively less attention has been devoted to labor market convergence in the post-crisis decade, particularly with explicit differentiation between crisis-adjustment and recovery phases.

Understanding unemployment convergence is especially relevant in the European context, where labor mobility, structural funds, fiscal surveillance, and coordinated policy responses aim to mitigate regional disparities. The post-2010 period provides a natural laboratory for examining whether crisis-induced divergence was followed by systematic mean reversion. If convergence mechanisms intensified during or after the crisis, this would suggest that EU integration frameworks contributed to labor market stabilization.

This study investigates unemployment convergence across the 27 EU member states over the period 2010–2019. Using annual panel data and a fixed-effects estimation strategy, the analysis tests for β-convergence in unemployment rates. Importantly, the study distinguishes between two sub-periods: the immediate post-crisis adjustment phase (2010–2013) and the subsequent recovery period (2014–2019). This distinction allows for an assessment of whether convergence dynamics differed between crisis stabilization and expansionary phases.

The findings indicate statistically significant unemployment convergence throughout the decade, with stronger adjustment dynamics during the crisis-adjustment phase and more moderate, yet persistent, convergence during the recovery period. These results contribute to the broader literature on European macroeconomic integration by providing evidence that labor market disparities narrowed in the aftermath of the crisis, albeit at varying speeds across phases.

The remainder of the paper is structured as follows. Section 2 reviews the relevant literature on convergence and labor market adjustment. Section 3 describes the data and variables. Section 4 outlines the empirical methodology. Section 5 presents the results. Section 6 discusses the implications of the findings, and Section 7 concludes.

2. Literature Review

The concept of convergence originates in the neoclassical growth framework, where economies are expected to approach their steady-state equilibria conditional on structural characteristics such as capital accumulation, demographic trends, and institutional quality (Barro & Sala-i-Martin, 1992, 2004). Early empirical studies introduced panel approaches that allowed for country-specific heterogeneity, providing evidence of conditional β-convergence within relatively homogeneous groups of economies (Islam, 1995). Subsequent contributions emphasized that convergence may not be universal and that multiple equilibria or threshold effects may generate persistent divergence across broader samples(Azariadis & Drazen, 1990; Durlauf & Johnson, 1995).

Beyond income convergence, the convergence framework has increasingly been applied to macroeconomic stability indicators and labor market outcomes. Labor market convergence is particularly relevant within monetary unions, where asymmetric shocks cannot be offset through exchange rate adjustments. Theoretical contributions highlight that labor mobility, wage flexibility, and fiscal transfers play central roles in mitigating regional disparities.

Empirical research on European convergence has produced mixed results. Some studies document partial income convergence among EU members, while others emphasize persistent structural heterogeneity between core and peripheral economies (Próchniak & Witkowski, 2012). Methodological advancements, particularly the time-varying factor model and log-t test introduced by Phillips and Sul (Phillips & Sul, 2007, 2009), demonstrated that full-sample convergence may be rejected even when subgroups of economies exhibit convergence patterns. This club-convergence perspective has influenced subsequent research on European macroeconomic dynamics.

The labor market dimension of convergence has received comparatively less systematic attention. Unemployment dynamics are often characterized by persistence and potential hysteresis effects, whereby temporary shocks may generate long-lasting structural impacts. Cross-country differences in labor market institutions, wage-setting mechanisms, and structural reform trajectories contribute to heterogeneous adjustment speeds. Empirical studies suggest that labor market integration within the EU remains incomplete, with substantial differences in unemployment levels and responsiveness to shocks across member states (Nickell et al., 2005).

The global financial crisis and the subsequent sovereign debt crisis introduced unprecedented asymmetries within the European Union. Southern European economies experienced dramatic surges in unemployment, while core economies maintained relatively stable labor markets. Research examining post-crisis macroeconomic adjustment highlights that periods of stress may trigger accelerated structural reforms and stronger policy coordination mechanisms. At the same time, divergence during crisis episodes may temporarily increase dispersion before convergence resumes during recovery phases.

Recent empirical contributions have revisited European convergence using updated panel datasets and refined econometric techniques. Studies focusing on income and institutional convergence within the EU and the Western Balkans provide evidence that convergence dynamics may vary across phases and structural groupings (Lalić & Trifunović, 2026b, 2026d, 2026c, 2026a). These analyses indicate that while full-sample convergence may appear modest, sub-period analyses often reveal stronger adjustment mechanisms during crisis or post-crisis stabilization phases. Related studies also emphasize the importance of digital transformation, human capital development, and sustainability-oriented policies as complementary factors supporting long-term socio-economic adjustment processes (Pajić et al., 2025; Bučalina Matić et al., 2024). Although primarily centered on income and institutional indicators, these findings suggest that convergence processes may intensify during periods of macroeconomic stress.

Institutional and macroeconomic credibility also play important roles in shaping adjustment dynamics. Regional academic contributions underline the structural constraints associated with institutional capacity and competitiveness (Anufrijev et al., 2026). Analyses of fiscal sustainability and monetary stabilization emphasize that disciplined macroeconomic frameworks support long-run adjustment and stability (Obućinski et al., 2025; Šare et al., 2026). Research on regulatory alignment and cross-border cooperation within Europe further suggests that institutional harmonization remains uneven between core and peripheral regions (Candida Bussoli & Ilenia Fraccalvier, 2025; Fejes, 2025). Knowledge and information management have increasingly been recognized as important determinants of organizational competitiveness and economic resilience (Mihajlović et al., 2024). While these studies do not directly test unemployment convergence, they provide contextual evidence of persistent structural heterogeneity that may influence labor market adjustment speeds.

Within this broader literature, unemployment convergence remains an underexplored dimension of European integration. Given the asymmetric nature of crisis shocks and the subsequent policy responses, distinguishing between crisis-adjustment and recovery phases may provide clearer insight into convergence dynamics. If labor markets exhibit mean reversion following macroeconomic stress, convergence may be stronger during adjustment periods and more moderate during expansionary phases. This study builds on the convergence tradition while focusing specifically on unemployment dynamics within the EU during the post-crisis decade.

3. Data and Variables

This study employs annual panel data covering the 27 member states of the European Union over the period 2010–2019. The selected time frame captures the post-sovereign debt crisis decade, allowing for the analysis of labor market adjustment during both the crisis-stabilization phase and the subsequent recovery period. Restricting the sample to EU member states ensures institutional comparability and avoids structural discontinuities associated with accession dynamics.

All macroeconomic variables are obtained from the World Bank’s World Development Indicators (WDI), ensuring cross-country consistency and methodological harmonization. The primary variable of interest is the unemployment rate, measured as the percentage of the total labor force. This indicator provides a standardized measure of labor market slack across member states and serves as the basis for testing convergence dynamics.

To examine β-convergence in unemployment, the empirical specification relies on the change in the unemployment rate as the dependent variable, constructed as the first difference of the annual unemployment rate. The lagged unemployment rate is included as the key explanatory variable. A negative and statistically significant coefficient on the lagged level indicates mean reversion and thus convergence in unemployment rates across countries.

In addition to the baseline specification, several macroeconomic controls are incorporated to account for cyclical and structural influences on labor market dynamics. Real GDP growth is included to capture aggregate demand conditions and cyclical fluctuations. Gross capital formation (as a percentage of GDP) serves as a proxy for domestic investment intensity and productive capacity expansion. In alternative specifications, additional macroeconomic variables such as foreign direct investment inflows and institutional quality indicators are introduced to assess robustness.

All variables are expressed in comparable units as provided by the World Bank database. The panel structure allows for the inclusion of country fixed effects to control for time-invariant national characteristics and year fixed effects to capture common shocks affecting all member states simultaneously. This framework isolates within-country adjustment dynamics and focuses on relative convergence rather than absolute cross-sectional differences.

Descriptive statistics indicate substantial heterogeneity in unemployment levels at the beginning of the sample period, reflecting the asymmetric impact of the crisis across EU member states. Over time, dispersion in unemployment rates declines, suggesting potential convergence during the recovery phase. These patterns motivate the formal econometric analysis presented in the subsequent sections.

4. Methodology

To examine unemployment convergence across EU member states, the empirical analysis is grounded in the β-convergence framework adapted to labor market dynamics. In this context, convergence implies that countries with higher initial unemployment rates experience stronger subsequent reductions in unemployment relative to countries with lower initial rates. Formally, convergence is tested by estimating the following specification:

![]()

where Ui,t denotes the annual change in the unemployment rate in country i at time t, Ui,t-1 represents the lagged unemployment rate, i captures country-specific fixed effects, t denotes year fixed effects, and i,t is the error term. A negative and statistically significant coefficient indicates mean reversion in unemployment rates and thus β-convergence across countries.

The inclusion of country fixed effects controls for time-invariant structural characteristics such as labor market institutions, demographic composition, and long-run policy frameworks. Year fixed effects capture common macroeconomic shocks, including EU-wide policy interventions and global economic fluctuations. This two-way fixed-effects framework focuses on within-country dynamics over time and eliminates bias arising from unobserved heterogeneity.

To assess conditional convergence, the baseline specification is extended by incorporating macroeconomic control variables:

![]()

where Xi,t includes real GDP growth and gross capital formation as proxies for cyclical demand conditions and investment dynamics. This extension allows the analysis to distinguish between pure mean reversion and convergence conditional on macroeconomic performance.

Given the potential presence of heteroskedasticity and cross-sectional dependence in macroeconomic panel data, standard errors are clustered at the country level in the baseline estimations. As an additional robustness check, Driscoll–Kraay standard errors are computed to account for cross-sectional correlation and temporal dependence in the residuals.

In order to examine whether convergence dynamics differed between phases of macroeconomic stress and recovery, the sample is divided into two sub-periods: the crisis-adjustment phase (2010–2013) and the recovery phase (2014–2019). The same β-convergence specification is estimated separately for each sub-period. This approach enables a direct comparison of adjustment speeds across phases and allows for the identification of potential structural shifts in labor market dynamics.

Finally, σ-convergence is assessed by analyzing the evolution of cross-country dispersion in unemployment rates over time. For each year, the standard deviation of unemployment across EU member states is calculated. A negative time trend in this dispersion measure indicates σ-convergence. The following regression is estimated:

![]()

where t represents the cross-sectional standard deviation of unemployment in year t. A negative and statistically significant coefficient provides evidence of declining dispersion and thus σ-convergence.

Together, the β- and σ-convergence approaches provide complementary perspectives on labor market integration. While β-convergence captures the speed of mean reversion in individual countries, σ-convergence reflects the evolution of overall cross-country dispersion. The combination of these methods allows for a comprehensive assessment of unemployment convergence within the European Union during the post-crisis decade.

5. Results

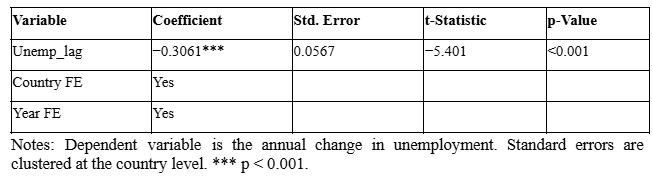

5.1 Full-Sample Unemployment β-Convergence (2010–2019)

The full-sample estimation provides strong evidence of unemployment β-convergence across EU member states during the period 2010–2019. The coefficient on the lagged unemployment rate is negative and highly statistically significant (-0.3061, p < 0.001), indicating substantial mean reversion.

Table 1. Unemployment β-Convergence, Full Sample (EU-27, 2010–2019)

The magnitude of the coefficient implies an annual adjustment speed of approximately 30 percent, suggesting that countries with higher initial unemployment rates experienced significantly faster reductions in unemployment growth compared to countries with lower initial rates. This result indicates a robust convergence process in labor market conditions across the European Union during the post-crisis decade.

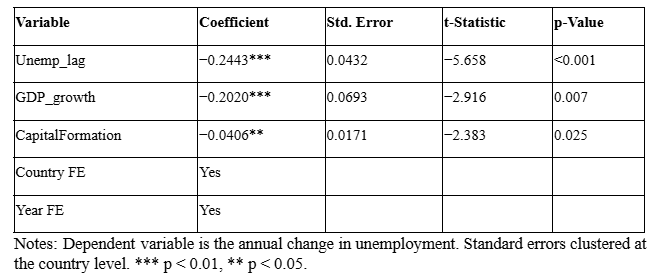

5.2 Conditional Unemployment Convergence

To assess whether convergence persists after controlling for macroeconomic conditions, the baseline specification is extended by including GDP growth and gross capital formation as control variables.

Table 2. Conditional Unemployment β-Convergence (Clustered Standard Errors)

The convergence effect remains negative and highly statistically significant after controlling for macroeconomic performance. The coefficient on the lagged unemployment rate (−0.2443) implies an annual adjustment speed of approximately 24 percent, confirming the robustness of unemployment convergence within the EU.

GDP growth exhibits the expected negative association with changes in unemployment, indicating that stronger economic performance contributes to faster reductions in unemployment. Gross capital formation is also negatively related to unemployment dynamics, suggesting that higher investment intensity is associated with improved labor market outcomes.

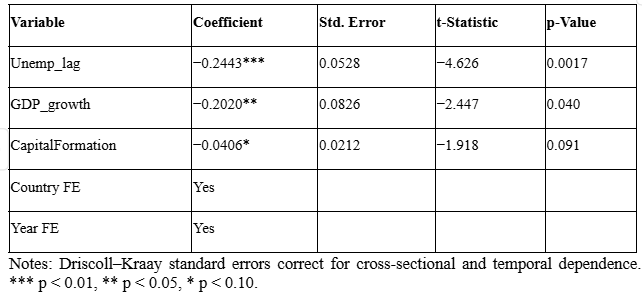

To further account for potential cross-sectional dependence and serial correlation, Driscoll–Kraay standard errors are reported in Table 3.

Table 3. Conditional Convergence (Driscoll–Kraay Standard Errors)

The results remain qualitatively unchanged under the more conservative error correction. The convergence coefficient remains negative and statistically significant at the 1 percent level. GDP growth continues to exert a statistically significant effect, while the investment variable becomes marginally significant at the 10 percent level.

Overall, the conditional specifications confirm that unemployment convergence in the European Union during 2010–2019 was not solely a mechanical mean reversion process, but was also associated with macroeconomic performance and investment dynamics.

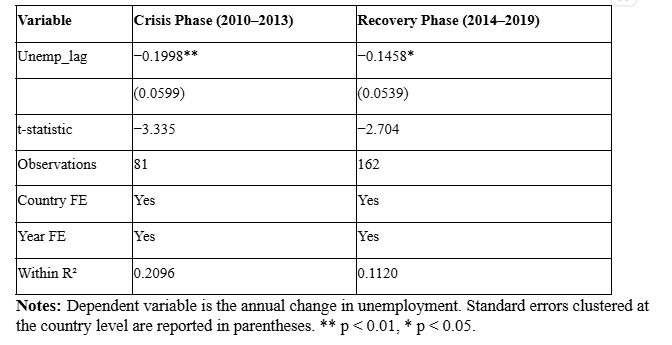

5.3 Phase-Specific Convergence: Crisis vs. Recovery

To examine whether convergence dynamics differed across macroeconomic phases, the sample is divided into two sub-periods: the crisis-adjustment phase (2010–2013) and the recovery phase (2014–2019). The same β-convergence specification is estimated separately for each period.

Table 4. Unemployment β-Convergence by Sub-Period

The results indicate statistically significant unemployment convergence in both sub-periods. During the crisis-adjustment phase (2010–2013), the estimated coefficient of −0.1998 implies an annual adjustment speed of approximately 20 percent. This suggests relatively rapid mean reversion in unemployment rates under conditions of macroeconomic stress.

In the recovery phase (2014–2019), convergence persisted but at a more moderate pace. The estimated adjustment speed of roughly 15 percent annually indicates that labor market equalization continued, although less intensively than during the crisis period.

The stronger convergence during the crisis-adjustment phase is consistent with the view that severe labor market imbalances triggered accelerated adjustment mechanisms. Countries experiencing sharp increases in unemployment during the sovereign debt crisis appear to have undergone faster corrective dynamics. During the recovery period, convergence remained present but proceeded through more gradual cyclical and structural channels.

Overall, the phase-specific analysis suggests that unemployment convergence in the European Union was not uniform across the decade. Instead, convergence dynamics were stronger during periods of macroeconomic stress and became more moderate once stabilization was achieved.

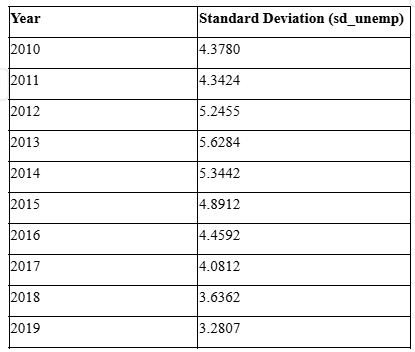

5.4 Sigma-Convergence in unemployment

While β-convergence evaluates whether countries with higher initial unemployment experience faster reductions, sigma-convergence examines whether cross-country dispersion in unemployment rates decreases over time. Sigma-convergence is assessed using the annual cross-sectional standard deviation of unemployment rates across EU Member States.

Table 5. Cross-Country Dispersion of Unemployment (σ) in the EU, 2010–2019

The negative coefficient on the time trend (−0.149) indicates a decline in cross-country unemployment dispersion of approximately 0.15 percentage points per year. Although statistical significance is at the 10 percent level (p ≈ 0.068), the magnitude and consistent downward pattern after 2013 provide supportive evidence of sigma-convergence during the latter part of the decade.

Taken together, the beta- and sigma-convergence results present a coherent picture. Unemployment rates converged both in terms of individual country adjustments (β-convergence) and in terms of reduced cross-country dispersion (σ-convergence), particularly during the post-crisis recovery phase.

6. Discussion

The empirical findings indicate that unemployment convergence in the European Union during 2010–2019 was present but phase-dependent. Absolute β-convergence results demonstrate statistically significant adjustment dynamics across Member States, suggesting that countries with initially higher unemployment rates experienced faster reductions over time. The estimated annual adjustment speed of approximately 20-30 percent implies a relatively meaningful process of labor market equalization within the Union.

However, the sub-period analysis reveals that convergence was not uniform throughout the decade. During the crisis-adjustment phase (2010–2013), convergence was stronger, indicating accelerated correction of extreme labor market imbalances. This pattern is consistent with the view that severe macroeconomic shocks may intensify adjustment mechanisms, either through structural reforms, labor market flexibility, or cyclical rebounds from sharp contractions.

In contrast, during the recovery phase (2014–2019), convergence persisted but at a more moderate pace. This suggests that once acute crisis pressures subsided, labor market dynamics evolved more gradually. The slower convergence in the recovery period may reflect structural heterogeneity in employment systems, productivity patterns, and demographic trends across Member States.

The conditional models further indicate that convergence was not purely mechanical mean reversion. GDP growth is consistently associated with reductions in unemployment, highlighting the role of macroeconomic performance in shaping labor market outcomes. Investment intensity also contributes to unemployment adjustments, although its significance weakens under more conservative standard error corrections. These results align with the broader macroeconomic literature emphasizing the importance of growth and capital accumulation in employment dynamics.

The sigma-convergence analysis complements these findings. Cross-country dispersion in unemployment increased during the sovereign debt crisis, peaking in 2013, and subsequently declined during the recovery. The trend regression confirms a gradual reduction in dispersion over the decade, albeit at moderate statistical significance. This pattern suggests that divergence during the crisis was followed by a process of re-alignment rather than persistent fragmentation.

Taken together, the results indicate that labor market convergence within the European Union is sensitive to macroeconomic conditions. Periods of systemic stress may temporarily widen disparities but can also trigger stronger adjustment dynamics. Conversely, stabilization periods are characterized by slower, more incremental convergence.

From a broader integration perspective, the findings suggest that the EU labor market framework - while lacking full fiscal and employment policy centralization - has exhibited a capacity for medium-term equalization following asymmetric shocks. However, convergence appears contingent on supportive macroeconomic environments rather than being an automatic structural outcome.

These results should be interpreted cautiously. The analysis covers a single decade and focuses exclusively on EU Member States. Moreover, while fixed-effects models control for time-invariant heterogeneity, they do not fully address potential structural breaks or deep institutional differences across national labor markets. Nonetheless, the consistency of β- and σ-convergence evidence strengthens the conclusion that labor market disparities narrowed during the post-crisis recovery phase.

7. Conclusion

This study examined unemployment convergence across the 27 member states of the European Union during the period 2010–2019. Using a fixed-effects panel framework and complementary dispersion analysis, the results provide consistent evidence of labor market convergence in the post-crisis decade.

The full-sample estimates indicate statistically significant β-convergence, suggesting meaningful mean reversion in unemployment rates across EU member states. Countries with higher initial unemployment levels experienced faster reductions in unemployment growth, contributing to gradual equalization. The estimated speed of adjustment implies that labor market disparities narrowed at a measurable annual rate.

Importantly, convergence dynamics differed across phases. During the crisis-adjustment period (2010–2013), convergence was stronger, reflecting accelerated correction of severe labor market imbalances. In the recovery phase (2014–2019), convergence persisted but at a more moderate pace. This phase-dependent pattern indicates that labor market equalization within the European Union is influenced by macroeconomic conditions and adjustment pressures.

The sigma-convergence analysis reinforces these findings. Cross-country dispersion in unemployment increased during the peak of the sovereign debt crisis but subsequently declined throughout the recovery period. This suggests that divergence during macroeconomic stress was not permanent and was followed by gradual re-alignment.

Overall, the evidence indicates that EU labor markets exhibited systematic convergence during the post-crisis decade. While convergence was not instantaneous, and disparities temporarily widened during the crisis, the medium-term trajectory points toward reduced unemployment differentials across member states.

From a policy perspective, the findings suggest that European labor market integration mechanisms - supported by macroeconomic coordination and structural adjustments - can contribute to stabilization following asymmetric shocks. However, convergence appears conditional on broader economic recovery rather than being fully automatic.

Future research may extend the analysis by incorporating longer time horizons, examining structural break effects, or exploring the role of institutional heterogeneity in shaping convergence speeds. Nonetheless, the present study provides empirical support for the presence of labor market convergence within the European Union during the decade following the sovereign debt crisis.

References

Azariadis, C., & Drazen, A. (1990). Threshold Externalities in Economic Development. The Quarterly Journal of Economics, 105(2), 501–526. https://doi.org/10.2307/2937797

Barro, R. J., & Sala-i-Martin, X. (1992). Convergence. Journal of Political Economy, 100(2), 223–251.

Barro, R. J., & Sala-i-Martin, X. (2004). Economic growth (2nd ed). MIT Press.

Bučalina Matić, A., Trifunović, D., & Blanuša, A. (2024). Značaj adekvatnog upravljanja otpadom i reciklaže u zaštiti životne sredine. Društveni horizonti, 3(7), 71–90. https://doi.org/10.5937/drushor2407071B

Candida Bussoli & Ilenia Fraccalvier. (2025, August 19). Circular Economy Disclosure in European Banks: A Substantive Commitment or Symbolic Compliance? Društveni Horizonti. https://drustveni-horizonti.fdn.edu.rs/articles/60

Durlauf, S. N., & Johnson, P. A. (1995). Multiple regimes and cross-country growth behaviour. Journal of Applied Econometrics, 10(4), 365–384. https://doi.org/10.1002/jae.3950100404

Fejes, Z. (2025, August 12). Evolution of Cross-Border Cooperation in the European Union – Challenges and Opportunities1. Društveni Horizonti. https://doi.org/10.5937/drushor2305055F

Islam, N. (1995). Growth Empirics: A Panel Data Approach*. The Quarterly Journal of Economics, 110(4), 1127–1170. https://doi.org/10.2307/2946651

Lalić, G., & Trifunović, D. (2026a). Economic and Institutional Convergence in Europe (2004–2023): EU Core, New Members, and the Western Balkans. Economies, 14(4), 142. https://doi.org/10.3390/economies14040142

Lalić, G., & Trifunović, D. (2026b). Income Convergence in Europe: The Role of Institutions and Structural Factors. Social Sciences, 15(3), 180. https://doi.org/10.3390/socsci15030180

Lalić, G., & Trifunović, D. (2026c). Institutional Quality as a Conditioning Factor of Convergence: Evidence from European Economies. World, 7(4), 51. https://doi.org/10.3390/world7040051

Lalić, G., & Trifunović, D. (2026d). Regulatory Volatility and Economic Growth in Europe: Heterogeneous Effects Across Institutional Development Stages. Sustainability, 18(5), 2658. https://doi.org/10.3390/su18052658

Nickell, S., Nunziata, L., & Ochel, W. (2005). Unemployment in the OECD Since the 1960s. What Do We Know? The Economic Journal, 115(500), 1–27. https://doi.org/10.1111/j.1468-0297.2004.00958.x

Mihajlović, M., Marković, S., Vujanić, I., Marijanović, R. P., & Ramadhani, I. H. (2024). Knowledge and information management in the company as a strategic business resource. Oditor, 10(3), 53–67. https://doi.org/10.59864/Oditor32403MM

Obućinski, D., Miljković, L., Ljubojević, N., & Krstić, S. (2025, November 26). THE ROLE OF MONETARY POLICY IN ENSURING MACROECONOMIC STABILITY. Oditor. https://doi.org/10.59864/Oditor42502SK

Pajić, S., Lalić, G., Trifunović, D., Maltez, K., & Jovanović, P. (2025). The influence of social networks on the teaching process of language learning. Oditor, 11(3). https://doi.org/10.59864/Oditor22503SP

Phillips, P. C. B., & Sul, D. (2007). Transition Modeling and Econometric Convergence Tests. Econometrica, 75(6), 1771–1855. https://doi.org/10.1111/j.1468-0262.2007.00811.x

Phillips, P. C. B., & Sul, D. (2009). Economic transition and growth. Journal of Applied Econometrics, 24(7), 1153–1185. https://doi.org/10.1002/jae.1080

Próchniak, M., & Witkowski, B. (2012). Real Economic Convergence and the Impact of Monetary Policy on Economic Growth of the EU Countries: The Analysis of Time Stability and the Identification of Major Turning Points Based on the Bayesian Methods (SSRN Scholarly Paper No. 2213712). Social Science Research Network. https://doi.org/10.2139/ssrn.2213712

Šare, D., Kosorić, D., & Tošev, D. (2025). THE IMPACT OF PUBLIC EXPENDIRURE AND PUBLIC DEBT ON ECONOMIC GROWTH DECLINE. Oditor. doi: 10.59864/Oditor 82503DS

Published in

Vol. 32 No. 1 (2026)

Keywords

Licence

This work is published under the Creative Commons Attribution 4.0 International (CC BY 4.0).

Authors retain copyright over their work.

Use, distribution, and adaptation of the work, including commercial use, is permitted with clear attribution to the original author and source.

Interested in Similar Research?

Browse All Articles and Journals