Impact of the implementation of the fatf recommendations on the financial performance of the gambling sector

Abstract

Implementation of the methodological framework of the Financial Action Task Force (FATF) is an international obligation of every country. One of the main objections to the FATF mechanism is that it ignores the costs of implementing the measures themselves. The largest number of scientific papers addressing the matter have pointed to the rise in operating expenses caused by the implementation of the recommendations, primarily by the operation of the AML function which is directly responsible for the implementation of standards at the individual obliged entity level. The aim of the paper is to analyse the impact of the implementation of the FATF recommendations and the expected standards on the financial performance of the sector participants, using the example of the gambling sector in the Republic of Serbia. The paper will assess the statistical significance of differences in the key business parameters but, unlike the majority of papers that exclusively focus on the impact of the FATF standards on the obliged entities’ operating costs, this study will analyse the effects on the entire business using composite indicators. Furthermore, in order to examine the impact of the implementation of the standards on the competitive position of the obliged entities in relation to neighbouring countries, the paper will test the statistical significance of the differences between these indicators in Serbia and the indicators of the same sector in Croatia and Slovenia.

Article

Introduction

The exceptionally adverse impact of the phenomena of money laundering, terrorism financing and the illicit proliferation on both the economic system and the society as a whole are the main drivers for creation of a uniform and systemic approach in addressing the issues on a global scale. The Financial Action Task Force (hereinafter referred to as ‘the FATF‘) is the creator of the policy to combat the phenomena on a worldwide scale. The system developed by the FATF is outlined through 40 Recommendations and eleven Immediate Outcomes (IO), forming the framework against which member systems' compliance with standards is assessed within the mutual evaluation system.

Unlike the early stages, contemporary mechanisms for combating money laundering, terrorism financing, and illicit proliferation are more comprehensive and demanding. Given that individual and bilateral approaches in addressing these issues have not yielded the expected results, it is clear that the multilateral approach plays an essential role in the success of the entire concept (Pavlidis, G. 2023).

The effectiveness of the implementation of the FATF recommendations depends on several factors, among which is the issue of limited resources of the private and public sectors One of the main objections to the FATF mechanism is that it ignores the costs of implementing the measures themselves. (Chaikin, D. 2009).

The risk avoidance policy (de-risking) is a direct adverse consequence of implementing the FATF measures, with numerous authors highlighting the potential to compromise the profitability of obliged entities as the main driver of the policy. Namely, high costs of the AML function (compliance function) for the obliged entities can have direct impact on reduction of profitability (Pavlidis, G. 2023).

The risk avoidance policy involves refusing to engage in business with a certain type of clients deemed high-risk in respect of money laundering or even refraining from any business activities with clients from high-risk regions, exemplified by Deutsche Bank's withdrawal from Malta and Latvia. An alternative to the policy would be conducting business subject to the due diligence principle and knowing and monitoring the customer albeit with the associated expenses that such activities entail (Rajnović, Lj. 2021).

The Swiss Banking Institute of the University of Zurich conducted a research on the implementation of FATF recommendations in the banking systems of Switzerland, Germany and Singapore. According to the aforementioned research, banks believe that the implementation of FATF recommendations is important for their operations, but that it is highly burdensome and causes significant costs in the entire banking sector (Geiger, H. Wuensch, O. 2007). According to the same research, the implementation of preventive measures to combat money laundering and terrorism financing accounts for 45% of the costs incurred due to legal obligations and 2% of the total costs for banks in Switzerland.

Additional legislative activities in this domain can be expected in the coming period, which will further intensify the pressure on the obliged entities’ AML function and undoubtedly lead to increased costs. Higher volume of information obtained by the obliged entities due to new legal obligations, insufficient comprehension of additional standard changes and the increasingly rigorous and demanding reporting needs are additional factors contributing to the rising costs of AML compliance (Thomson Reuters. 2023; (Rajnović, Lj., Bukvić, R. 2017).

The FATF framework classifies participants in the gambling sector, especially casinos, in the category of obliged entities that are required to apply all preventive measures and actions subject to special conditions for their establishment and operation. In addition to financial institutions, accountants, lawyers, auditors, notaries public, real estate agencies, and gem dealers, gambling service providers serve as the 'guardians' of the economic system against the inflow of dirty money.

Providing gambling services is one of the most profitable businesses. Some authors highlight that the expansion of the industry, in addition to illegal and unregulated online betting, has been significantly influenced by the liberalisation of the conditions for establishing and operating such platforms (Järvinen- Tassopoulos, J. 2022). On the other hand, a certain number of authors emphasize the special treatment given to this industry from tax and regulatory perspective, primarily due to the problem of gambling addiction it generates and, consequently, the social costs incurred by that problem. (Paldam, M. 2008).

The segment of online games of chance, measured by earned revenue, has an annual growth rate of 10.2% and is estimated to reach USD 133 billion worldwide in 2026. The European region accounts for 52.1% of the global online betting market. (Marketline.2022).

There is a consensus in academia that the gambling sector is an under-researched field, with few scientific papers offering solutions to numerous unresolved issues. The largest number of papers deals with the financial aspect of the sector and mathematical settings of the model itself (Liston, D.P. Gutierrez Pineda J.P. 2020).

In the period 2018-2020, the Republic of Serbia fully harmonised its regulations in the field of games of chance with the FATF standards and expected results. With the adoption of the new Law on Games of Chance (Official Gazette of RS, No. 18/2020) and the establishment of the Games of Chance Administration, the system of the Republic of Serbia has been fully aligned with FATF Recommendation 28.

Considering the aforementioned, the paper aims to examine how the implementation of the FATF recommendations and the expected standards affects the financial performance of sector participants, illustrated by the gambling sector in the Republic of Serbia. The statistical significance of differences in basic business parameters, such as indicators of profitability, productivity and stability before and after the introduction of standards in the sector, will be compared. Unlike the majority of papers that exclusively focus on the impact of the FATF standards implementation on the obliged entities’ operating costs, this paper will analyse the effects on the entire business using composite indicators. Additionally, the paper will test the statistical significance of the differences between these indicators in Serbia and those of the corresponding sector in Croatia and Slovenia, with the aim of examining the impact of implementing the standards on the competitive position of the obliged entities relative to the neighbouring countries, providing a more comprehensive perspective on the issue presented.

Characteristics of the Gambling Sector in the Republic of Serbia

Under the Law on Games of Chance (hereinafter referred to as: ‘the Law’), there are three categories of games of chance: classic games of chance, special games of chance and prize games in goods and services (Article 13 of the Law). Regarding classic games of chance, there is one registered legal entity – the State Lottery of Serbia. As far as the special games of chance are concerned, in accordance with Article 15 of the Law, they include: 1) games of chance in gaming houses; 2) games of chance on gaming machines; 3) betting games; 4) games of chance through means of electronic communication (online games of chance). All gambling service providers are registered in the form of limited liability company.

Operators of special games of chance in gaming houses and those operating games of chance through means of electronic communication are obliged entities subject to Article 4 of the Law on the Prevention of Money Laundering and the Financing of Terrorism (Official Gazette of RS, Nos. 113/2017, 91/2019, 153/2020 and 92/2023).

The legal framework in this area has been significantly improved, as it established all the legal prerequisites for preventive action to combat money laundering, terrorism financing and illicit proliferation in the sector. The conditions for granting licences to operators have been further restricted. The circle of entities that must meet the so-called "fit and proper" standards has been expanded. Of particular significance is the possibility of losing the licence in case of acting in contravention of the regulations governing prevention of money laundering and terrorism financing. With the aforementioned amendments, Serbia has implemented all the recommendations proposed by the Council of Europe's Committee (MONEYVAL) to comply with the FATF recommendations. (MONEYVAL. 2016).

The sector was assessed on three occasions regarding exposure to the risks of money laundering and terrorism financing, with the latest evaluation conducted in 2021. That year, the Government of Serbia adopted the National Money Laundering and Terrorism Financing Risk Assessment. Rating the gambling sector as high-risk has primarily been influenced by the criminal proceedings initiated against 19 gambling service providers’ employees for the criminal offense of money laundering (NRA. 2021). Additionally, as a typological characteristic of money laundering through the sector, cash payments based on games of chance winnings lacking any proof of winnings have been detected (Radovanović, Ž. et al.). 2023). The risk assessment finds that, in addition to the gambling sector, accountants and the real estate sector are the most vulnerable.

Research Methods

The data on the number of companies and the balance sheet positions of the gambling sector in Serbia, Croatia and Slovenia for the nine-year observation period, from 2014 to 2022, have been taken from the Orbis database. The balance sheet positions are expressed in EUR.

Table 1 Financial data of the Gambling Sector in the R. of Serbia

|

|

Years |

||||||||

|

2022 th EUR |

2021 th EUR |

2020 th EUR |

2019 th EUR |

2018 th EUR |

2017 th EUR |

2016 th EUR |

2015 th EUR |

2014 th EUR |

|

|

Operating revenue (Turnover) |

916,997 |

588,455 |

470,550 |

768,974 |

566,647 |

417,736 |

373,629 |

443,968 |

350,311 |

|

P/L before tax |

135,357 |

53,699 |

34,022 |

78,570 |

41,464 |

44,075 |

20,618 |

8,900 |

-8,801 |

|

P/L for period [=Net income] |

94,738 |

47,417 |

23,193 |

65,257 |

33,631 |

36,788 |

17,375 |

7,691 |

-8,015 |

|

Cash flow [Net Income before D&A] |

167,562 |

98,170 |

34,947 |

86,386 |

42,274 |

50,477 |

28,399 |

16,047 |

996 |

|

Total assets |

554,262 |

419,509 |

288,850 |

225,835 |

188,868 |

156,510 |

129,587 |

93,871 |

103,045 |

|

Shareholders funds |

233,384 |

171,435 |

152,218 |

129,925 |

41,117 |

30,068 |

4,790 |

-15,308 |

-9,042 |

|

Current ratio (x) |

0.86 |

0.78 |

0.95 |

1.09 |

1.10 |

1.28 |

1.22 |

1.30 |

1.25 |

|

Profit margin (%) |

14.80 |

9.20 |

7.34 |

10.25 |

7.33 |

10.55 |

5.52 |

2.01 |

-2.50 |

|

ROE using P/L before tax (%) |

57.07 |

34.08 |

25.73 |

60.14 |

43.47 |

47.61 |

37.03 |

26.78 |

32.40 |

|

ROCE using P/L before tax (%) |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

|

Solvency ratio (Asset based) (%) |

42.11 |

40.87 |

52.70 |

57.53 |

21.77 |

19.21 |

3.70 |

-16.31 |

-8.78 |

|

Number of employees |

15,324 |

13,550 |

13,326 |

12,546 |

11,451 |

10,057 |

6,547 |

6,549 |

7,036 |

Source: Orbis database (2024)

Table 2 Financial data of the Gambling Sector in the R. of Croatia

|

|

Years |

||||||||

|

2022 th EUR |

2021 th EUR |

2020 th EUR |

2019 th EUR |

2018 th EUR |

2017 th EUR |

2016 th EUR |

2015 th EUR |

2014 th EUR |

|

|

Operating revenue (Turnover) |

690,175 |

509,267 |

482,038 |

523,679 |

479,906 |

415,491 |

325,710 |

240,845 |

243,271 |

|

P/L before tax |

147,290 |

88,500 |

92,397 |

119,356 |

110,504 |

75,927 |

47,028 |

37,091 |

48,416 |

|

P/L for period [=Net income] |

111,098 |

70,070 |

72,207 |

96,158 |

90,332 |

60,690 |

39,946 |

28,157 |

47,324 |

|

Cash flow [Net Income before D&A] |

155,930 |

116,555 |

119,830 |

145,693 |

122,590 |

89,817 |

62,139 |

39,335 |

56,506 |

|

Total assets |

619,041 |

597,673 |

539,278 |

541,939 |

474,480 |

370,991 |

311,830 |

259,314 |

168,906 |

|

Shareholders funds |

253,276 |

238,647 |

260,539 |

261,418 |

228,094 |

214,100 |

169,397 |

138,931 |

81,312 |

|

Current ratio (x) |

1.41 |

1.29 |

1.40 |

1.62 |

1.52 |

2.14 |

1.91 |

2.27 |

2.23 |

|

Profit margin (%) |

21.34 |

17.38 |

19.17 |

22.80 |

23.03 |

18.27 |

14.44 |

15.43 |

19.96 |

|

ROE using P/L before tax (%) |

52.47 |

36.08 |

36.75 |

45.54 |

47.25 |

34.53 |

29.07 |

25.38 |

58.56 |

|

ROCE using P/L before tax (%) |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

n.a. |

|

Solvency ratio (Asset based) (%) |

40.91 |

39.93 |

48.31 |

48.24 |

48.07 |

57.71 |

54.32 |

53.58 |

48.14 |

|

Number of employees |

7,199 |

7,113 |

7,443 |

7,344 |

7,158 |

6,995 |

6,299 |

5,460 |

5,417 |

Source: Orbis database (2024)

Table 3 Financial data of the Gambling Sector in the R. of Slovenia

|

|

Years |

||||||||

|

2022 th EUR |

2021 th EUR |

2020 th EUR |

2019 th EUR |

2018 th EUR |

2017 th EUR |

2016 th EUR |

2015 th EUR |

2014 th EUR |

|

|

Operating revenue (Turnover) |

422,525 |

323,885 |

293,539 |

382,334 |

360,918 |

263,214 |

185,278 |

286,207 |

267,059 |

|

P/L before tax |

31,113 |

8,745 |

-2,403 |

18,484 |

14,182 |

15,041 |

10,167 |

25,655 |

11,288 |

|

P/L for period [=Net income] |

26,708 |

6,981 |

-3,675 |

16,748 |

11,980 |

7,523 |

4,370 |

17,277 |

10,156 |

|

Cash flow [Net Income before D&A] |

46,342 |

28,019 |

19,925 |

38,836 |

34,283 |

13,402 |

9,388 |

38,727 |

31,413 |

|

Total assets |

275,033 |

263,838 |

247,543 |

266,535 |

267,877 |

251,048 |

228,736 |

263,757 |

281,922 |

|

Shareholders funds |

130,449 |

117,770 |

115,406 |

110,282 |

115,493 |

95,821 |

75,590 |

119,260 |

109,993 |

|

Current ratio (x) |

1.16 |

0.82 |

0.77 |

0.76 |

1.04 |

0.86 |

0.79 |

1.03 |

0.96 |

|

Profit margin (%) |

7.36 |

2.77 |

-0.81 |

4.83 |

3.93 |

5.71 |

5.49 |

8.96 |

4.23 |

|

ROE using P/L before tax (%) |

23.70 |

7.52 |

-1.35 |

16.71 |

12.28 |

15.69 |

13.45 |

21.50 |

10.25 |

|

ROCE using P/L before tax (%) |

16.68 |

5.95 |

-1.43 |

13.39 |

7.32 |

7.79 |

6.25 |

14.50 |

5.60 |

|

Solvency ratio (Asset based) (%) |

47.43 |

44.64 |

46.62 |

41.38 |

43.11 |

38.17 |

33.05 |

45.22 |

39.02 |

|

Number of employees |

1,877 |

1,919 |

2,098 |

2,042 |

2,028 |

1,984 |

1,788 |

1,799 |

1,979 |

Source: Orbis database (2024)

Statistical hypothesis testing using the T test of independent groups will be conducted on the example of operating income, rate of return on assets, net profit rate, and current ratio. Previous research on corporate-level financial performance have been based on the mentioned indicators, so the proposed framework is fully aligned with empirically verified methodological framework and the best practice (Mihailović, N. Radovanović, Ž. Radovanović S. 2023).

Additionally, the paper builds upon the results of previous research on this topic.

A group of authors analysed the gambling sector in the territory of Croatia. The Croatian gambling market, a small but dynamic segment of the Croatian economy, is characterised by high concentration. Namely, the five largest companies generated 70% of the sector's revenue. From a negative profit margin in 2009, the sector achieved an average profit margin of 15% in 2017. (Šimović, H. et al. 2019).

Findings and Conclusions

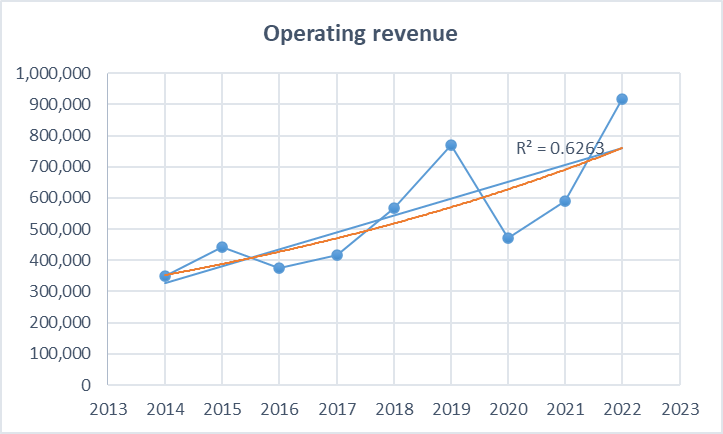

In 2014, the Serbian gambling sector comprised of 57 companies that generated the total operating revenue of about EUR 350 million. The sector had 7,035 employees. Until 2019, the rate of income growth exhibited an almost exponential progression. In 2019, the year that preceded the introduction of the reforms, 72 companies generated revenue of EUR 769 million. In addition to doubling revenue, the sector also doubled its number of employees, reaching 12,546 that year.

In the year when the reforms were introduced, i.e. when the new licencing and business system was established, with full compliance of the aforementioned processes with the FATF recommendations, the sector generated revenue of EUR 470.5 million, marking a nearly 39% decline in the sector's revenues. At the same time, there was an increase in the number of companies, from 72 to 76 and the number of employees, from 12,546 to 13,326.

In the very next year, the sector once again recorded an increase in revenues, reaching EUR 588.5 million in 2021. 66 companies operated in the sector, marking a 13% decrease compared to the previous year, with 13,550 employees.

In 2022, the sector recorded a growth rate of 55.8% compared to the previous year, with revenues reaching a record value of nearly EUR 917 million. Moreover, the sector saw its peak with a total of 79 companies operating, employing 15,324 individuals.

As depicted in Graph 1, the revenue of the gambling sector exhibits an upward trend.

Graph 1 Operating Revenue (EUR '000)

Source: Authors' calculation

To ascertain the presence of a pattern in revenue movement, we will test statistical hypotheses:

H0: There is no tendency in revenue movements, i.e. the observed variations in the time series are merely random.

Ha: The tendency in revenue movements is statistically significant, i.e. the observed variations in the time series are not merely random.

Applying the Mann-Kendall test returns the following results:

|

Kendall's tau |

0,643 |

|

S |

18 |

|

Var(S) |

65,333 |

|

p-value (Two- tailed) |

0,035 |

|

alpha |

0,05 |

As the calculated p-value is lower than the significance level (α), we reject the null hypothesis and accept the alternative, indicating that the tendency in revenue movement is statistically significant and the observed variations in the time series are not merely random. The trend exhibits a strong upward tendency.

Drawing from the test results, it can be inferred that the implemented reforms, primarily aimed at harmonisation with the FATF recommendations, did not exert a long-term negative impact on the revenue of the Serbian games of chances sector.

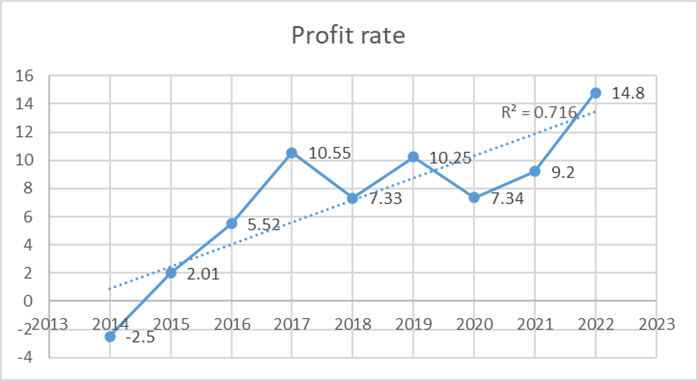

To assess the impact of the implemented reforms on the sector's business performance, the same test was conducted on the example of the profit rate, and its trend is illustrated in Graph 2.

Graph 2 Profit rate of the Gambling Sector in Serbia

Source: Authors' calculation

We will define the null and alternative hypothesis:

H0: There is no tendency in profit rate movements, i.e. the observed variations in the time series are merely random.

Ha: The tendency in profit rate movements is statistically significant, i.e. the observed variations in the time series are not merely random.

Applying the Mann-Kendall test returns the following results:

|

Kendall's tau |

0,571 |

|

S |

16 |

|

Var(S) |

65,333 |

|

p-value (Two- tailed) |

0,043 |

|

alpha |

0,05 |

As the calculated p-value is lower than the significance level (α), we reject the null hypothesis and accept the alternative, indicating that the tendency in profit rate movement is statistically significant and the observed variations in the time series are not merely random. The trend exhibits a strong upward tendency.

Drawing from the test results, it can be inferred that the implemented reforms, primarily aimed at harmonisation with the FATF recommendations, did not exert a negative impact on profit rate movements in the Serbian gambling sector.

The test results confirmed strong upward trend of the sector’s profit rate and revenue. However, it is important to investigate whether the reforms had an adverse impact on other financial indicators of the sector, potentially indicating a less favourable position compared to competing companies in the immediate environment.

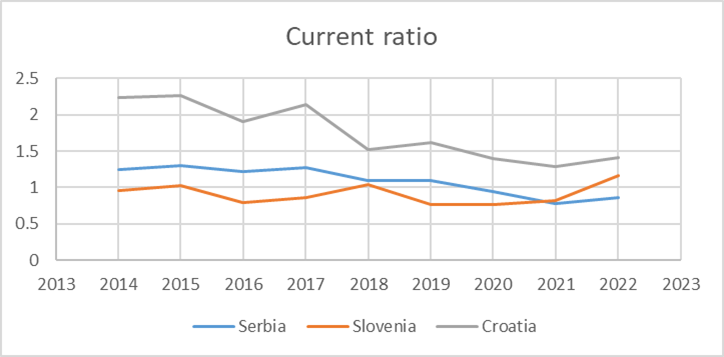

Graph 3 illustrates the comparative movement of the current liquidity ratio in the gambling sectors of Serbia, Croatia and Slovenia.

Graph 3 Comparative Overview of Current Ratio in Serbia, Croatia and Slovenia

Source: Authors' calculation

The current liquidity ratio shows the relationship between current assets and current liabilities, that is, the ability to cover current liabilities with current assets. By analysing the indicator's movements, it can be concluded that its value in the sector in Serbia fluctuates around 1, as is the case in Slovenia. The value of this indicator is slightly higher in Croatia, ranging from 1.29 to 2.23, although it exhibits a downward trend. Analysis of the current liquidity ratio reveals a slight downward trend in the games of chances sector in Serbia. Based on the movement of this indicator, no conclusion can be drawn regarding the impact of the reforms in the Republic of Serbia during 2020 that would exert a strong negative effect on the level of current liquidity ratio in the sector and its less favourable position compared to the neighbouring countries.

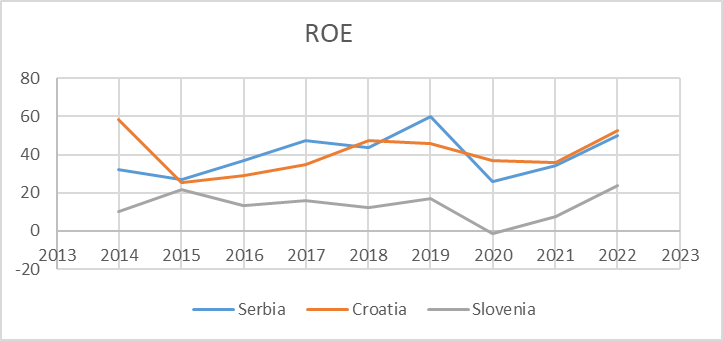

Graph 4 shows the development of the rate of return on equity (ROE), as an indicator of equity investment profitability.

Graph 4 Comparative Overview of ROE in Serbia, Croatia and Slovenia

Source: Authors' calculation

By analysing ROE over time, it can be concluded that the return on equity in Serbia and Croatia is at a significantly higher level compared to Slovenia. In 2019, ROE had the highest value in Serbia, while in 2020 its value fell below that in Croatia. In 2021 and 2022, its values in Serbia and Croatia were almost identical. Based on the movement of this indicator, a conclusion can be drawn about the short-term impact of the reforms in the Republic of Serbia during 2020, leading to a decline in the value of the ROE indicator. However, no conclusions can be drawn indicating a long-term adverse effect of the reforms on the ROE indicator, considering its subsequent growth in the following years and the fact that the indicator is at the same level as in Croatia.

References

2. FATF (2012-2019). International Standards on Combating Money Laundering and the Financing of Terrorism & Proliferation. FATF. Paris. France.

www.fatf-gafi.org

3. Geiger, H. Wuensch, O. 2007. The fight against money laundering -An economic analysis of a cost-benefit paradoxon, Journal of Money Laundering Control Vol. 10 No. 1, 2007. Emerald Group Publishing Limited. https://www.apml.gov.rs/nacionalna-procena-rizika- 1000000259

4. Järvinen-Tassopoulos, J. (2022). State-Owned Gambling Operation in a Global Competitive Environment. In: Nikkinen, J., Marionneau, V., Egerer, M. (eds) The Global Gambling Industry. Glücksspielforschung. Springer Gabler, Wiesbaden.

5. Liston, D.P. Gutierrez Pineda J.P. 2020. Financial Performance of Internet Gambling Stocks: Empirical Evidence from the UK. Review of Integrative Business and Economics Research, Vol. 9, Issue 3. GMP Press and Printing.

6. MarketLine. 2022. Global Online Gambling Market Summary, Competitive Analysis and Forecast, 2017-2026. https://store.marketline.com/report/global-overview-of- online-gambling-market-and-analysis/

7. Mihailović, N. Radovanović, Ž. Radovanović S. 2023. Comparative financial analysis of fruit and vegetable juice production sectors in Serbia and Croatia. Economics of Agriculture Vol LXX, No3 (677-924).

8. MONEYVAL. 2016. Anti-money laundering and counter-terrorist financing measures – Serbia. Fifth Round Mutual Evaluation Report. Council of Europe. Committee of experts on the evaluation of anti-money laundering measures and the financing of terrorism (MONEYVAL).

9. Orbis database (2024) www.bvdinfo.com

10. Paldam, M. (2008). The Political Economy of Regulating Gambling. In: Viren, M. (eds) Gaming in the New Market Environment. Palgrave Macmillan, London.

11. Pavlidis, G. (2023). The dark side of anti-money laundering: Mitigating the unintended consequences of FATF standards. Journal of Economic Criminology 2 (2023).

12. Radna grupa za izradu Nacionalne procene rizika od pranja novca i nacionalne procene rizika od finansiranja terorizma. Urednik: Pantelić,J. 2021. Nacionalna procena rizika od pranja novca i nacionalna procena rizika od finansiranja terorizma. Vlada R Srbije.

13. Radovanović, Ž i dr. 2023. Tipologije pranja novca. Ministarstvo finansija Uprava za sprečavanje pranja novca. Misija OEBS u Srbiji. ISBN-978-86-81546-12-3. COBISS.SR-ID 132105481

14. Rajnović, Lj., 2021. Ugovori u privredi sa osvrtom na eksterne uticaje na ugovorni odnos, Institit za ekonomiku poljoprivrede Beograd, ISBN 978-86-6269-106—4: eISBN 978-86-6269-107-

1.

15. Rajnović, Lj., Bukvić, R. (2017) – Monografija: Korporativno upravlјanje kao deo poslovne strategije kompanija, Institut za ekonomiku polјoprivrede, Beograd, Srbija, 2017, ISBN 978-86- 6269-057-9.

16. Šimović, H. Bajo, A. Primorac, M. Davidović, M. Jelavić, F. 2019. Gambling Market in Croatia: Financial Performance and Fiscal Effect, Fiscus: prudent and responsible public sector financial management, 2019. 4, 1 – 32. Institute of Public Finance. https://doi.org/10.3326/efiscus.2019.9

17. Thomson Reuters. 2023. Cost of Compliance - Regulatory burden poses operational challenges for compliance. Thomson Reuters Regulatory Intelligence. https://legal.thomsonreuters.com/content/dam/ewpm/docum ents/legal/en/pdf/reports/cost-of-compliance-report-final- web.pdf

18. Zakon o igrama na sreću ("Sl. glasnik RS", br. 18/2020)

19. Zakon o sprečavanju pranja novca i finansiranja terorizma („Sl.glasnik RS“, br. 113/2017,91/2019,153/2020 i 92/2023)

Published in

Vol. 30, No. 1, 2024.

Keywords

Licence

This work is published under the Creative Commons Attribution 4.0 International (CC BY 4.0).

Authors retain copyright over their work.

Use, distribution, and adaptation of the work, including commercial use, is permitted with clear attribution to the original author and source.

Interested in Similar Research?

Browse All Articles and Journals